Angola’s Credit Allocation (2020–2025): Growth Without Transformation?

FGSC Consulting

22 May 2026

Angola’s Credit Allocation (2020–2025): Growth Without Transformation?

FGSC Consulting Research – Macroeconomic & Financial Sector Analysis

Executive Summary:

Between 2020 and 2025 Angola’s banking system saw a massive expansion of credit (nearly doubling from Kz 4.6 to 8.9 trillion). However, the allocation of this credit raises concern. Most lending has flowed into trade, consumption, and government financing, rather than productive or social sectors. By end-2025, over 65% of credit went to wholesale/retail trade (import‐related), households (consumer credit), construction, and public administration. In contrast, sectors crucial for diversification – agriculture, manufacturing, human capital (education/health), and infrastructure (water/sanitation) – remain underfinanced. This pattern reflects Angola’s oil-dependent, import-driven growth model[1][2] and poses clear risks: low long-term growth, high vulnerability to shocks, and persistent development gaps.

Building on BNA sectoral data and international studies, this analysis provides a detailed, sector-by-sector diagnosis, highlighting the mismatch between credit flows and development needs. We conclude with the long-term risks of this credit structure and policy priorities (financing agriculture, SMEs, human capital, etc.) to steer Angola towards diversification and resilience.

We analyze official BNA data (absolute credit stocks and sectoral shares for 2020–2025) alongside IMF, World Bank, African Development Bank, INE, and CEIC reports on Angola. Key steps included: (1) Verifying BNA figures from published tables; (2) Computing growth rates and concentration measures; (3) Reviewing literature on Angola’s economy, including national plans (NDP/PRODESI) and sector studies. All statements are supported by up-to-date sources (2022–2026). Where data is missing, we explicitly note it.

Credit Growth vs. Economic Structure

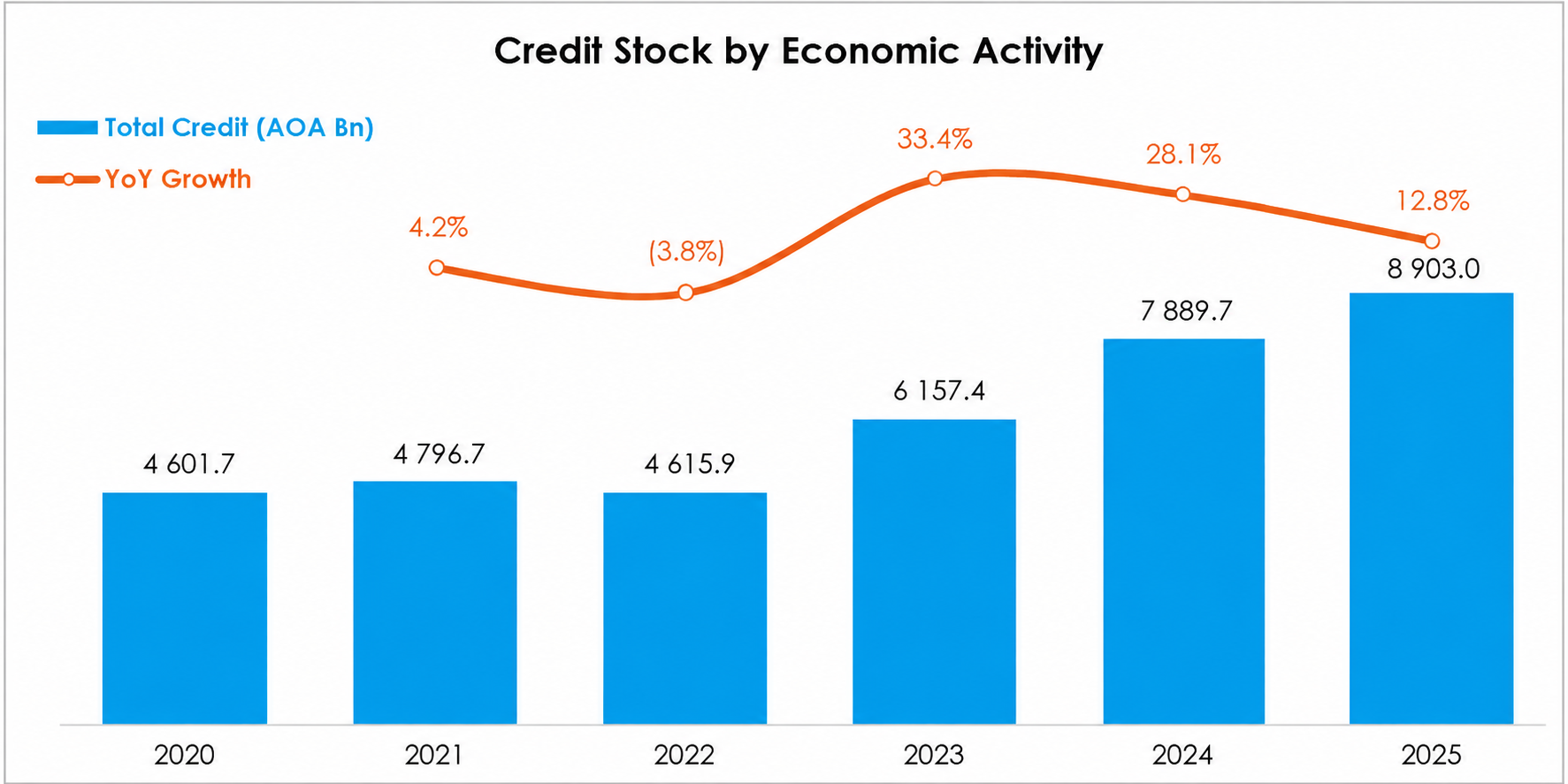

Figure 1: Total bank credit to the non‑financial sector in Angola. (Source: BNA data)

Credit roughly doubled from 2020 to 2025. This surge (especially +33% in 2023, +28% in 2024) reflects looser monetary conditions and inflation-driven expansion, after a fiscal/monetary adjustment period in 2021–22. However, overall credit penetration remains low: private credit is only c.6% of GDP (2023)[3], far below Sub-Saharan peers. The IMF notes that Angola’s credit-to-GDP has been “below the SSA average” for two decades[3]. Banks have ample liquidity, but lending remains constrained by high inflation, risk, and collateral shortages[3].

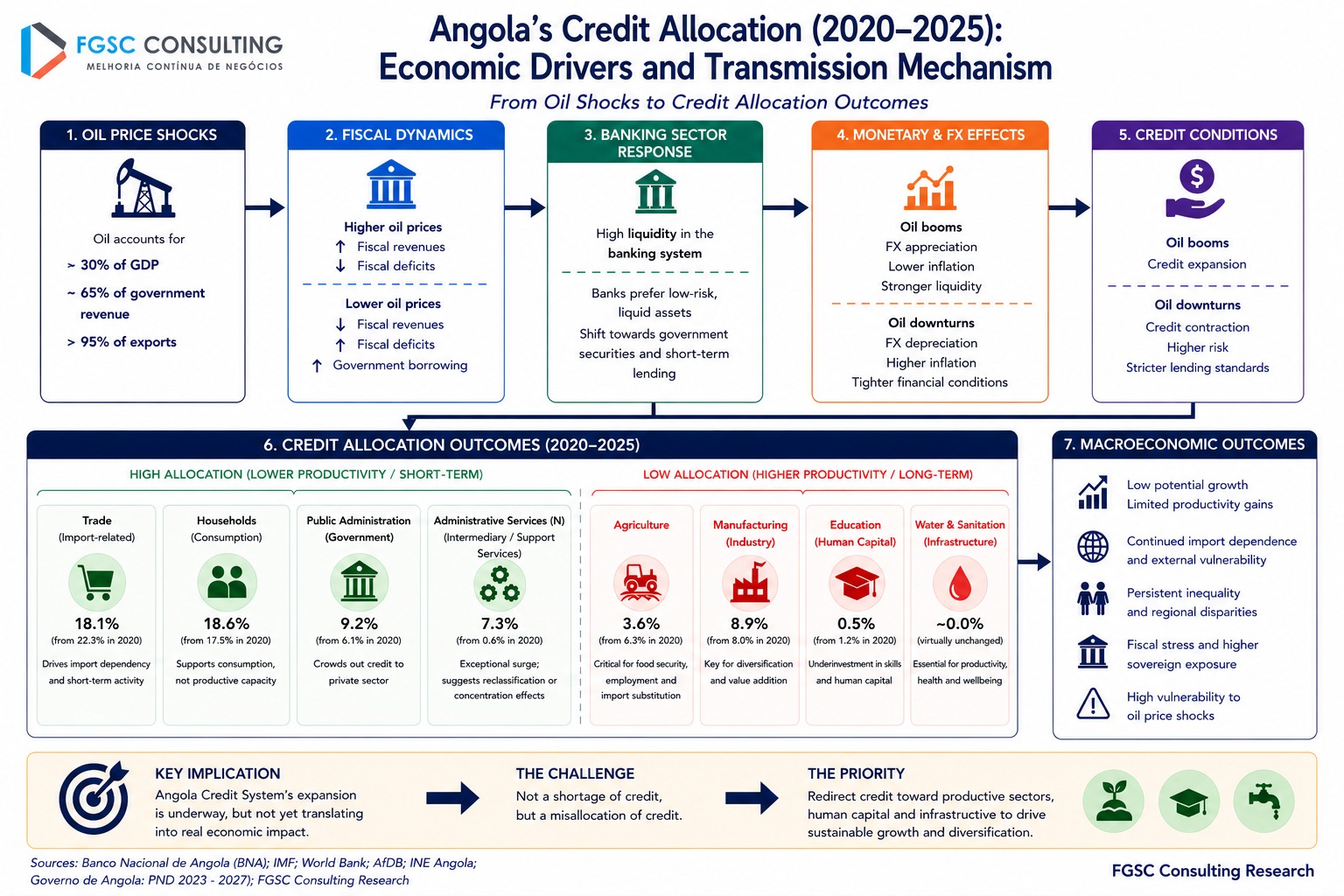

As context, Angola’s economy is still oil-dominated. Oil accounts for c.30% of GDP and c.65% of government revenue[1], and more than 95% of exports. Oil price swings drive fiscal and exchange-rate volatility, which undermines credit stability[4][1]. These macro factors shape banks’ behavior: during oil booms, credit can expand, but usually into short-term trade and consumption, not long-term investment.

Oil price volatility directly translates into fiscal and exchange rate instability, which in turn affects credit conditions. During periods of high oil prices, increased fiscal revenues and foreign exchange inflows support liquidity in the banking system, enabling credit expansion. However, this expansion is typically directed toward short-term trade financing and consumption, rather than long-term productive investment.

Conversely, during oil price downturns, declining revenues lead to fiscal tightening, increased government borrowing, currency depreciation, and inflationary pressures. These dynamics reduce real incomes, increase credit risk, and constrain both the supply and demand for credit

Figure 2: Stylized flow of Angola’s credit allocation (2020–2025) and economic drivers.

Sectoral Credit Breakdown

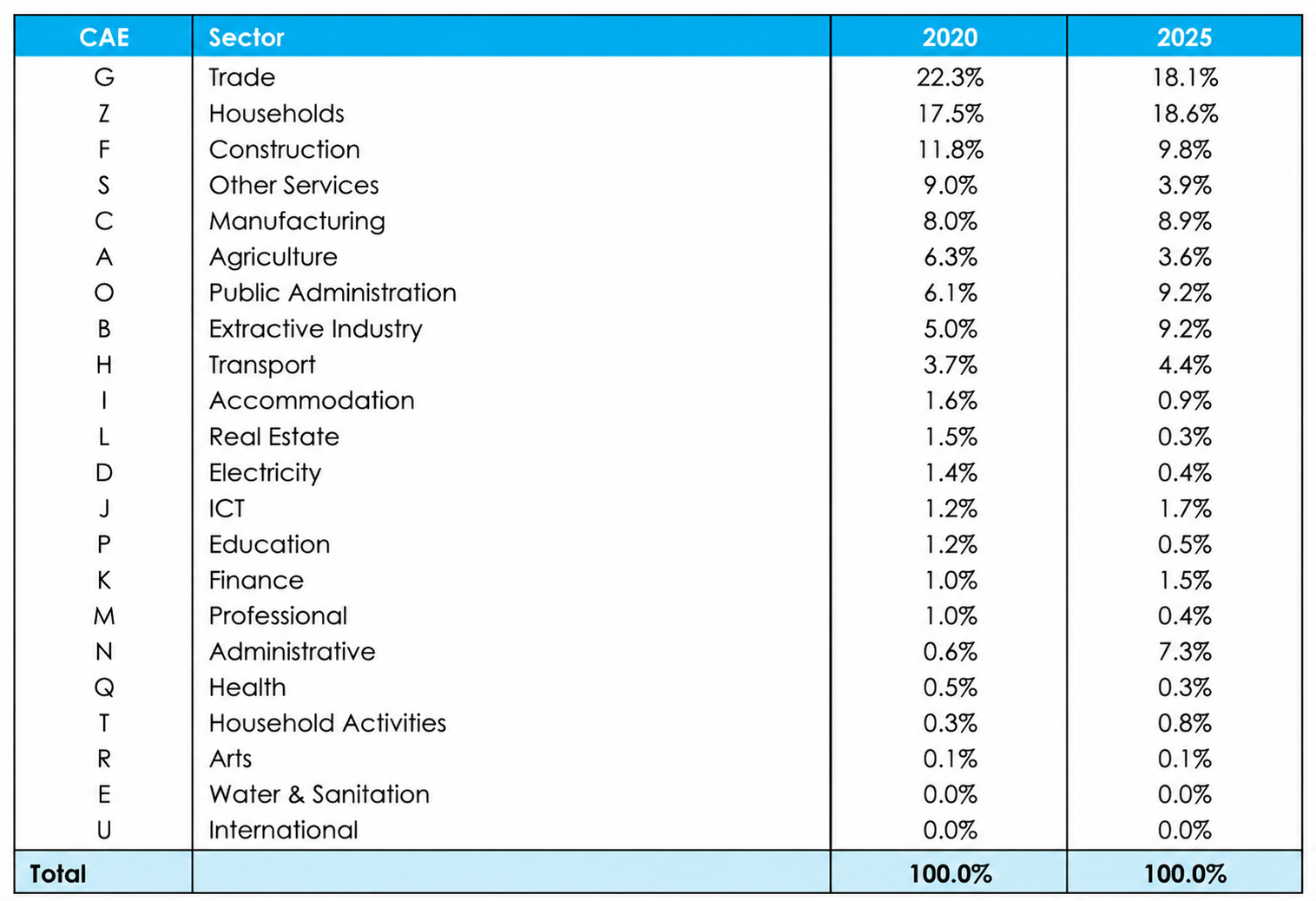

The composition of credit reveals its structural bias. Table 2 summarizes the shift from 2020 to 2025 (sectors defined by BNA’s CAE classification).

Table 1: Share of total bank credit by sector, 2020 vs 2025. (Source: BNA data)

Key observations:

- Trade & Household consumption dominate: In 2025, trade (wholesale/retail) and household credit alone comprised c.37% of all credit, down slightly from c.40% in 2020. These sectors include working capital for import-dependent trade and consumer loans.

- Public sector borrowing surged: Public administration’s share jumped from 6.1% to 9.2%. Banks now hold a much larger portion of government debt (public sector credit was AOA 1.4 trn by Mar 2026, 67% of which was central government[5]). IMF warns this “sovereign‑bank nexus” risks crowding-out private investment[3].

- Weakening of productive sectors: Manufacturing’s share ticked up only slightly (+0.9 pts) despite more than doubling in absolute terms; agriculture’s share halved (6.3%→3.6%). These subsectors are underfunded relative to their development importance (NDP targets boosting agri’s GDP share from 8.6% to 10.3% by 2027[6]).

- Neglected human capital & infrastructure: Education and health each absorb <1% of credit (education dropped to 0.5%). Water/sanitation is essentially zero. These sectors are funded mainly by donors/budget, not bank loans.

Overall, c.70–80% of credit (by share) now goes to just five areas: trade, households, construction, public administration, and manufacturing. Even so, only a minority of that reaches production: in March 2026, credit to the “real economy” (producer sector) was Kz 2.0 trn, just c.22% of total credit[7]. The rest finances imports, consumption, and government.

Sectoral Analysis

- Trade (Wholesale & Retail Commerce)

2020: AOA 1,024.6 bn (22.3%) 2025: AOA 1,615.9 bn (18.1%) up 58%.

Trade credit remains the largest single slice of the pie. This reflects Angola’s import-heavy economy: retailers and importers borrow to finance inventory. While this supports consumption, it has low multiplier effects on domestic output. The World Bank notes Angola’s growth is “concentrated in non‑tradables” like trade[1]. High trade credit also underscores FX vulnerability: more imports mean more exchange-rate exposure.

- Households (Consumer Loans)

2020: AOA 806.4 bn (17.5%) 2025: AOA 1,660.3 bn (18.6%) up 106.

Consumer credit has more than doubled. Driven by rising incomes (oil-related wage hikes) and pent-up demand, banks have expanded retail lending. This fuels growth in the short run (via consumption) but raises risks: inflationary pressure and higher delinquency if incomes sag. Commercial banks like BAI and BFA report retail lending is a key profit driver. The IMF highlights Angola’s low savings rate and informal economy as a credit barrier, but households saw the largest absolute credit stock increase.

- Construction

2020: AOA 543.4 bn (11.8%) 2025: AOA 875.8 bn (9.8%) 61%.

Construction lending jumped with Angola’s public and private building boom. The government has invested heavily in infrastructure (roads, ports, housing) under the NDP. However, banks focus on project finance for state-backed projects. Risk: a credit cycle tied to government spending. A slowdown in public works could leave many loans underutilized.

- Manufacturing (Industries Transformadoras)

2020: AOA 368.5 bn (8.0%) 2025: AOA 791.3 bn (8.9%) up 115%.

Manufacturing credit more than doubled, reflecting some new private investments in agro-processing and light industry. Yet, at under 9% of total lending, industry remains a secondary priority for banks. Angola’s industrial base is still underdeveloped (INE data show low industrial diversification). Banks cite high operational risks and poor collateral when avoiding manufacturing. In practice, many industrial projects rely on development finance or public incentives, not commercial bank loans.

- Agriculture, Livestock, Forestry, Fishing

2020: AOA c.289 bn (6.3%) 2025: AOA c.320 bn (3.6%) up 11%.

Financial support for agriculture is scant. Despite being a policy priority (e.g., NDP and “Planagrão” target a growing food sector[6]), credit to agriculture stagnated in absolute terms and halved in share. The small increase masks a large decline in priority. Agricultural producers cite lack of collateral and rural outreach as obstacles. This misalignment is stark given Angola’s food import reliance and the official goal of expanding agriculture to c.10% of GDP by 2027[6].

- Public Administration (Government & State Enterprises)

2020: AOA 279.7 bn (6.1%) 2025: AOA 818.1 bn (9.2%), up 193%.

Government borrowing from the banking sector has skyrocketed. By Mar 2026, banks held AOA 1.4 trn of public (non-financial) debt, of which 67% was the central government[5]. This reflects fiscal strains: in 2025 Angola spent c.46% of its budget on debt service (mostly domestic)[8][5]. The crowding-out effect is real: private sector credit (firms & households) grew only c.12% y/y by Mar 2026[9], far below government borrowing. The IMF explicitly warns that high government debt “may potentially crowd out lending to the private sector”[3].

- Transport & Logistics

2020: c.AOA 170 bn (3.7%) 2025: c.AOA 392 bn (4.4%) up 130% est.

Lending to transport, warehousing, and logistics is small but growing. Much of this is fueled by strategic projects (e.g., rail/road to Lobito Corridor). Financing remains dominated by public-private partnerships. Given Angola’s geography, strengthening logistics is essential for diversification, but banks are cautious about heavy capex in this sector without guaranteed returns.

- Information & Communication (ICT)

2020: c.AOA 55 bn (1.2%) 2025: c.AOA 151 bn (1.7%) up 174% est.

Interestingly, ICT credit saw the highest growth rate (albeit on a small base). The government’s digital agenda (e.g., e-government, fintech reforms) seems to have spurred some corporate borrowing. Still, ICT remains more than 2% of credit, indicating that tech businesses rely mostly on equity/FDI.

- Underserved Sectors: Social and Basic Services

The most striking gaps are in sectors vital for long-run human development and resilience. Banks have virtually ignored these areas:

- Education: Credit share fell from 1.2% to 0.5%. The only financing is typically donor-driven or state budget. Angola has one of the lowest education metrics in SSA (Human Capital Index c.0.36[10]). The recent World Bank/MIGA debt-for-education swap (USD 400 m, 2026) underscores this failure of domestic finance: only through creative debt reduction can Angola free funds for new schools[8][11].

- Health: Remains under 0.5%. Public health infrastructure is largely built by the state. Notably, in 2026 the BNA mandated banks to extend credit to health/pharma (hospitals, clinics, medicines)[12]. This policy move itself signals that private lending was negligible.

- Water & Sanitation: Essentially 0% of credit. Major urban water projects rely on foreign loans (e.g. WB’s $150m loan in 2018[13]). Access to clean water is low, and sanitation even lower. The lack of commercial financing in this sector means Angola depends on donors and state budgets for basic utilities.

These sectors are critical for sustainable growth. Poor health and education limit labor productivity; inadequate water/sanitation fuels disease and infrastructure bottlenecks. The World Bank explicitly links Angola’s challenges to “limited access to basic infrastructure and low human capital”[14]. The fact that formal credit virtually bypasses these areas suggests financial markets are neglecting human capital and public goods entirely.

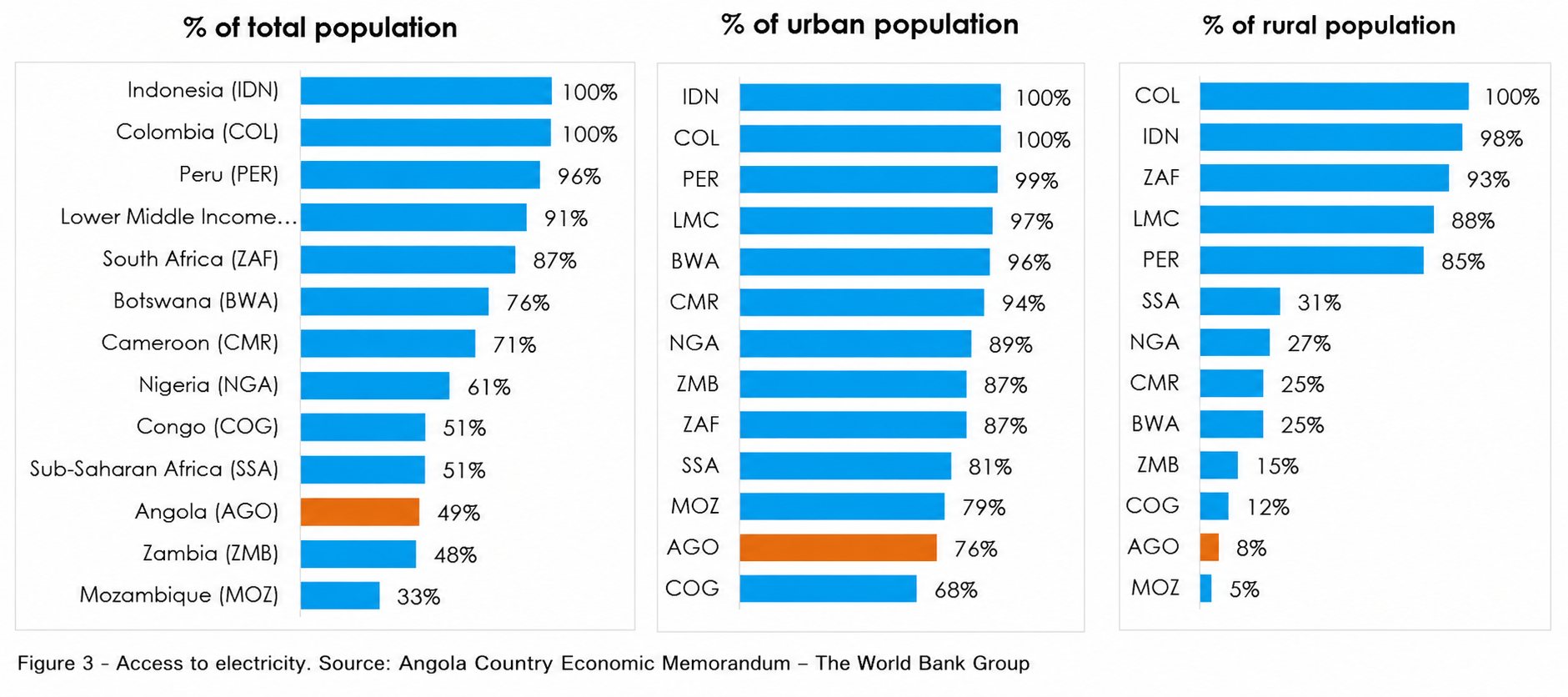

Electricity Access Constraint - Access to electricity (total, urban, rural) in Angola and peers, 2022

Structural constraints in infrastructure further explain the weak transmission of credit into productive sectors. Access to electricity remains limited, particularly outside urban areas. According to World Bank data, only around 45% of the population had access to electricity in 2022, with a sharp urban–rural divide (urban access above 70%, rural access below 10%). This gap reflects limited transmission and distribution infrastructure, which increases operating costs and reduces the viability of industrial and agricultural investment.

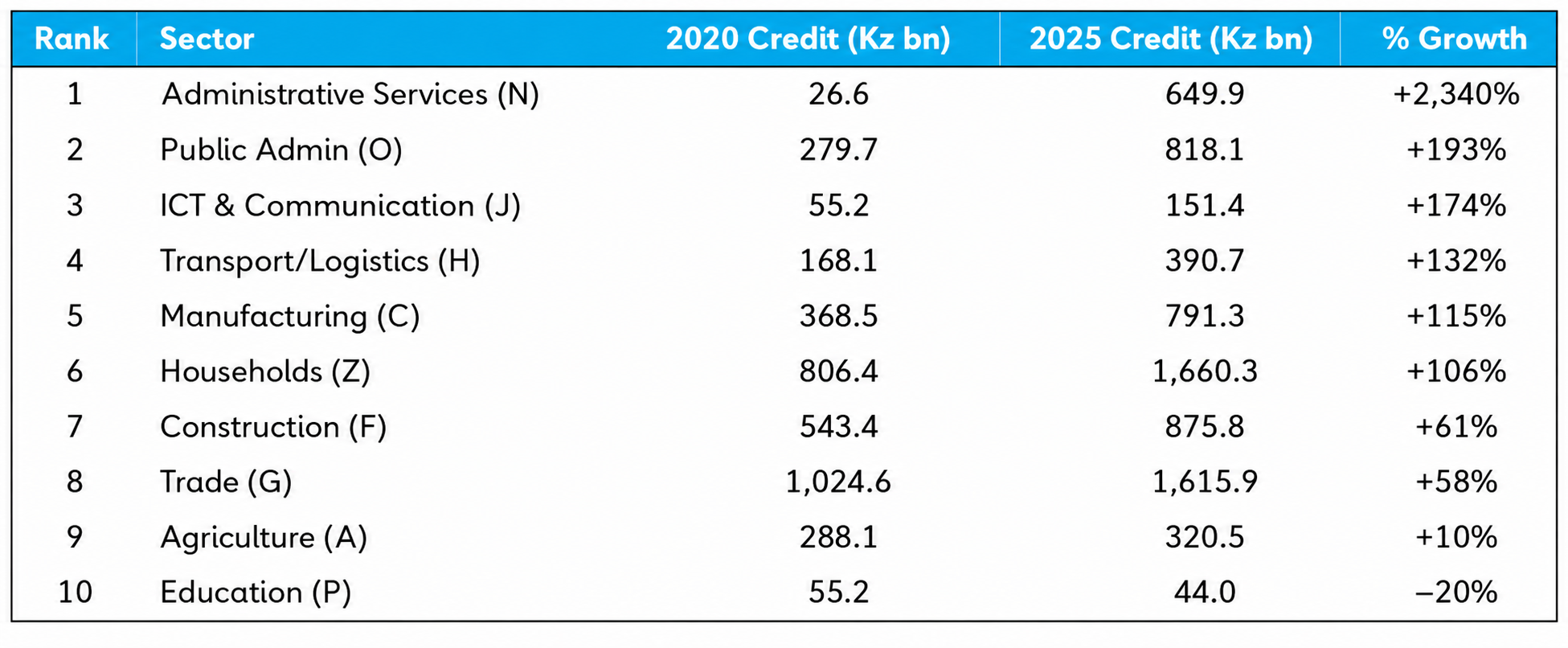

Fastest Growing Credit Segments (2020–2025)

To highlight the divergences, Table 2 ranks sectors by credit growth.

This highlights several structural anomalies. Education contracted in credit terms, while agriculture saw only marginal growth, underscoring weak support for foundational development sectors. In contrast, the credit expansion disproportionately benefited public administration, households, ICT, and transport.

Most notably, Administrative Services recorded an exceptional surge, suggesting possible reclassification effects or increased concentration of intermediary activities rather than organic sectoral growth. While part of the ICT increase may reflect post-pandemic digital demand, the broader pattern is clear: credit growth is concentrated in sectors with limited direct impact on long-term productivity and structural transformation.

Long-Term Risks of Current Allocation

Angola’s credit patterns embed several systemic risks:

- Stalled Diversification: Persistent funding to trade/consumption perpetuates an oil-and-imports economy. Without capital flowing into industry, agriculture, and innovation, non-oil GDP growth will remain modest. The IMF and World Bank stress that diversification is key to stability[4][15].

- Credit Misallocation: High exposure to low-productivity sectors weakens the impact of credit on economic potential. Angola’s credit-to-GDP is already very low[3]; if even that small pie favors consumption and public debt, long-term output suffers.

- Fiscal-Banking Feedback: The sharp rise in public sector lending ties banks’ health to government debt. A negative oil shock or fiscal crisis could force banks to absorb losses, undermining financial stability. In fact, by early 2026, c.15.6% of banking assets were government loans[5].

- Social Underinvestment: Neglecting education, health, water means Angola risks a weak human capital foundation. This slows productivity growth and traps poverty. (About one-third of Angolans live under $2.15/day[16].)

- Vulnerability to Shocks: With credit fueling imports, Angola is susceptible to currency swings. A weaker kwanza (in part caused by past oil deficits) raises debt burdens for importers, potentially triggering defaults.

In sum, growth may continue, but it will likely be uneven, import-driven, and volatile. The nation’s debt sustainability and poverty-reduction goals are at risk if these credit patterns persist.

Policy Implications and Recommendations

Angola needs to rebalance credit flows in line with its development strategy (NDP/PRODESI). Key priorities should include:

- Incentivize Productive Lending: Strengthen credit lines or guarantee schemes targeting agriculture (e.g. agri-VC funds[17]), manufacturing, and SMEs. The NDP already calls for easier finance, and IMF suggests expanding credit bureaus and collateral options[18]. Public guarantees or interest subsidies for strategic projects (e.g. agro-processing plants, smallholders) can lower bank risk.

- Deepen Rural Finance: Expand branch/agency networks and microfinance in rural areas. Provide land-titling reforms so farmers can use farmland as collateral (as prioritized by NDP). Donor-supported funds (e.g. FAO, AfDB programs) can be leveraged to crowd in private loans.

- Enhance Financial Sector Regulation: The BNA should continue measures to ensure banks diversify portfolios (beyond government bonds). It could set prudent ceilings on sovereign exposure or risk-weight public debt more heavily. Strengthening bank supervision (as recommended by IMF[18]) will improve credit quality.

- Channel Foreign Funds to Gaps: Use debt-for-development swaps and concessional loans (like the education swap[8] and MIGA-backed projects) to finance public goods. But always pair with reforms to stimulate domestic financing. For example, combine the water sector loan[13] with reforms to attract private water utilities.

- Support Human Capital & Infrastructure: Ensure budget and donor funds cover education/health but also create blended finance vehicles for these sectors. E.g., PPPs for schools and hospitals, or social bonds could be explored. The debt-for-education deal is a step; similar creativity (debt-for-health, etc. as hinted in [22]) is needed.

- Promote Export-Capable Projects: Encourage lending to export-oriented production (industrial parks, logistics corridors). For instance, credit to transport/logistics (currently c.4%) could be increased via public-private initiatives, given the Lobito Corridor's potential[19].

By redirecting finance toward these areas, Angola can reinforce the positive drivers of growth: diversification, productivity, and resilience. The long-term payoff is higher, more stable GDP growth and poverty reduction[4][20].

Conclusion

Angola’s banking sector today has liquidity and credit capacity. The problem is where that credit goes. Current allocation is imbalanced: overwhelmingly to consumption, trade, and government debt, rather than to the sectors that build the nation’s future.

In the words of the World Bank: “excessive dependence on oil…has not helped develop a strong private sector”[21]. The data show a financial system that has scaled up without structurally transforming. Angola does not have a fundamental shortage of credit, it has a credit allocation problem. Without decisive policy shifts to steer funds into agriculture, industry, education, and infrastructure, the economy will remain vulnerable and slow-growing.

Addressing this requires top-down support for financial reforms (as IMF & NDP suggest[18][6]) alongside targeted programs. Only then can Angola’s fast-growing credit markets translate into broad-based, sustainable development.

References (selected):

Banco Nacional de Angola; IMF Country Report No. 25/63 (2025)[3]; World Bank Angola Economic Update (2023)[1]; World Bank Angola CEM (2025)[20]; FAO/Angola agri sector plan (2023)[6]; Novo Jornal (Apr 2026)[5]; Reuters/360 news (Angola debt-for-education, 2026)[8][11]; World Bank press (water project, 2018)[13]; 360 Mozambique (BNA health credit 2026)[12].

[1] [10] [14] [15] [16] [20] [21] Angola Country Economic Memorandum: Moving Beyond Oil (https://www.worldbank.org/en/country/angola/publication/angola-country-economic-memorandum-moving-beyond-oil)

[2] [6] [17] Ag. sector overview (https://www.fao.org/media/docs/handinhandlibraries/countries/angola/apresenta%C3%A7%C3%A3o-angola---26-09-2023-2.pdf?sfvrsn=9684d942_1)

[3] [4] [18] Angola: Selected Issues; IMF Country Report No. 25/63; February 6, 2025 (https://www.imf.org/-/media/files/publications/cr/2025/english/1agoea2025002-print-pdf.pdf)

[5] [7] [9] BNA: Crédito bruto ao sector não financeiro atingiu 9,0 biliões kz em Março de 2026, um crescimento de 16,4 % face ao período homólogo (https://novojornal.co.ao/economia/detalhe/bna-credito-bruto-ao-sector-nao-financeiro-atingiu-90-bilioes-de-kwanzas-em-marco-de-2026-um-crescimento-de-164-face-ao-periodo-homologo-71449.html)

[8] [11] Angola: World Bank Guarantees Debt Swap to Finance Education 360 Mozambique (https://360mozambique.com/world/angola/angola-world-bank-guarantees-debt-swap-to-finance-education/)

[12] Angola: BNA Extends Bank Credit to Health and Pharmaceutical Industry Sectors • 360 Mozambique (https://360mozambique.com/world/angola/angola-bna-extends-bank-credit-to-health-and-pharmaceutical-industry-sectors/)

[13] Angola: World Bank Approves $150 Million to Improve Water Services (https://www.worldbank.org/en/news/press-release/2018/06/21/angola-world-bank-approves-150-million-to-improve-water-services)

[19] Angola - Country Economic Memorandum : Moving Beyond Oil - Laying the Foundations for Growth and Jobs (https://documents.worldbank.org/en/publication/documents-reports/documentdetail/099072425042515440)

#AngolaEconomy #CreditAllocation #AngolaBankingSector #EconomicDiversification